연말 평가에 얼마나 많은 의미를 부여해야 할까요?

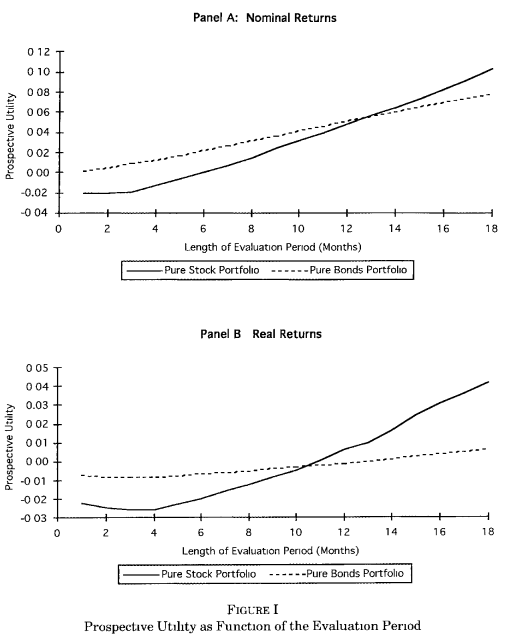

“극도로 훈련된 전문 투자자들도 연말 평가에 비합리적으로 큰 의미를 부여합니다. 수십년 짜리 장기 금융상품에는 장기 수익률이 높은 주식만 들어있어야 하는데, 장기 수익률이 낮은 채권도 포함되어 있습니다. 이러한 이해할 수 없는 현상을 조사해보니, 투자자들이 근시안적 손실 회피 (Myopic loss aversion) 성향을 보이기 때문에 단기 수익률에는 차이가 없는 주식과 채권의 수익률을 해마다 확인하기 때문이라고 합니다. 전문 투자자도 인간이라서 1년이라는 단기적 관점에서 벗어나기 어렵나 봅니다”

*행동경제학

연말 결산을 바라보는 다양한 시각

– #연말결산 과 연단위 계획, 꼭 필요할까?

– 장기 계획의 중요성과 투자를 위한 조언 등

– #주재우 교수 (국민대 경영학과) #KBS1라디오 #경제라디오 #성공예감이대호입니다 #성공예감 #이대호

***

Reference

Benartzi, S., & Thaler, R. H. (1995). Myopic loss aversion and the equity premium puzzle. The Quarterly Journal of Economics, 110(1), 73-92.

The equity premium puzzle refers to the empirical fact that stocks have outperformed bonds over the last century by a surprisingly large margin. We offer a new explanation based on two behavioral concepts. First, investors are assumed to be “loss averse,” meaning that they are distinctly more sensitive to losses than to gains. Second, even long-term investors are assumed to evaluate their portfolios frequently. We dub this combination “myopic loss aversion.” Using simulations, we find that the size of the equity premium is consistent with the previously estimated parameters of prospect theory if investors evaluate their portfolios annually.